In partnership with

The outbreak of war is a profoundly unsettling event, marked by human tragedy, geopolitical upheaval, and deep-seated uncertainty. The intuitive response for any investor is one of fear—a primal urge to de-risk portfolios and flee to safety. The imagery of conflict seems fundamentally incompatible with the orderly function of capital markets. Yet, a rigorous examination of over a century of financial history reveals a striking and persistent paradox: while armed conflict is terrifying and destructive, the stock market often demonstrates a surprising, and at times even robust, resilience.

This article will dissect this complex relationship, moving beyond the simplistic narrative that "war is bad for stocks." The central thesis is that market outcomes are not dictated by the moral or emotional weight of a conflict, but by its tangible impact on the underlying fundamentals of the economy. Factors such as the pre-existing economic environment, the nature and scale of government fiscal responses, the effect on inflation and monetary policy, and the disruption to critical commodity markets are the true drivers of performance. War, in this context, acts not as a direct cause of market behavior, but as a powerful and unpredictable catalyst that can either amplify existing trends or trigger a fundamental economic regime change.

Don’t snooze on student loans

June is the sweet spot to start planning how you’ll cover what FAFSA doesn’t.

You’ve got time to compare options, talk it over with a co-signer, and find a private loan that actually fits your life.

Think beyond tuition—the right student loan can cover housing, meal plans, and even your laptop.

View Money’s best student loans list to find a lender, apply in as little as 3 minutes, and start the semester on the right foot.

The initial reaction to geopolitical shocks is almost invariably negative. The eruption of conflict injects a massive dose of uncertainty into the global system, prompting investors to sell equities and seek refuge in traditional safe-haven assets like gold, government bonds, and stable currencies. However, historical data consistently shows that this knee-jerk sell-off is often short-lived. An extensive analysis of major geopolitical events since the 1940s by LPL Financial found that the S&P 500's average drawdown was a relatively modest 5%, with a full recovery typically occurring in less than 50 days.1 A similar study by Deutsche Bank found that geopolitical sell-offs tend to be followed by a recovery that is just as rapid, with the S&P 500 typically regaining all losses within three weeks.2

More remarkably, over the full duration of some of history's most devastating conflicts, U.S. markets have posted significant gains. During World War II, a conflict of unparalleled scale and destruction, the Dow Jones Industrial Average — $DJI ( ▲ 0.27% ) rose a cumulative 50% from 1939 to 1945. This counterintuitive performance gives rise to what researchers have termed "the war puzzle"—the phenomenon where markets, after an initial period of fear, often stabilize and even rally in the face of what appears to be grim certainty.

This article will explore that puzzle in exhaustive detail. It will demonstrate that the common narrative of "market resilience" is an oversimplification. This resilience is not a uniform market characteristic but a historically contingent outcome. The key determinant of whether a geopolitical shock leads to a brief dip or a sustained bear market is whether the conflict acts as a net economic stimulant or a stagflationary drag. A war that unleashes massive fiscal spending into a depressed economy, as World War II did for a United States emerging from the Great Depression, is fundamentally different from a conflict that triggers a commodity price shock in an already inflationary environment, as the 2022 invasion of Ukraine did. The market is not resilient to war per se; it is resilient to shocks that do not ultimately cause a recession.3

By conducting a historical autopsy of major conflicts, dissecting the causal economic mechanisms, and analyzing the evolving nature of warfare in the 21st century—including the critical new frontiers of trade and cyber conflict—this report will provide a definitive framework for understanding and navigating one of the most challenging environments for any investor.

A Historical Autopsy of Markets at War

To understand the present and anticipate the future, one must first dissect the past. The relationship between war and stock market performance is not governed by a single, immutable law but has evolved over time, shaped by the unique economic, political, and technological context of each conflict. This historical analysis will establish the empirical foundation of this report, examining market behavior from the total wars of the early 20th century to the regional and asymmetric conflicts of the modern era.

World War I (1914-1918)

The outbreak of the Great War in the summer of 1914 was a profound shock to a globalized financial system that had known relative peace for decades. The reaction was immediate and chaotic. As European nations scrambled to liquidate foreign assets to finance their war efforts, a massive liquidity crisis ensued. The Dow Jones Industrial Average plummeted by approximately 30%, and in an unprecedented move to prevent a complete collapse, the New York Stock Exchange (NYSE) was closed on July 31, 1914. It would not fully reopen for six months, the longest such shutdown in its history.

Year | DJIA Annual Return (%) | Key Events5 |

1914 | -30.72% | Outbreak of war; NYSE closes for six months |

1915 | +81.66% | NYSE reopens; U.S. industrial boom supplying Allies |

1916 | -4.19% | Market consolidation after massive gains |

1917 | -21.71% | U.S. enters the war |

1918 | +10.51% | War concludes; market rallies on victory |

When the market reopened in December 1914, however, the narrative had already shifted dramatically. With the United States officially neutral, its industrial base became the primary supplier to the Allied powers. This influx of war orders ignited an economic boom. The result was one of the most powerful rallies in market history. In 1915, the DJIA surged an astonishing 88%, a record for a single-year gain that still stands today. Over the entire course of the war, from 1914 to its conclusion in late 1918, the Dow gained a total of 43%, which translates to a healthy annualized return of 8.7%.4 This established the first key precedent: for a non-combatant industrial power, war elsewhere can be exceptionally profitable.

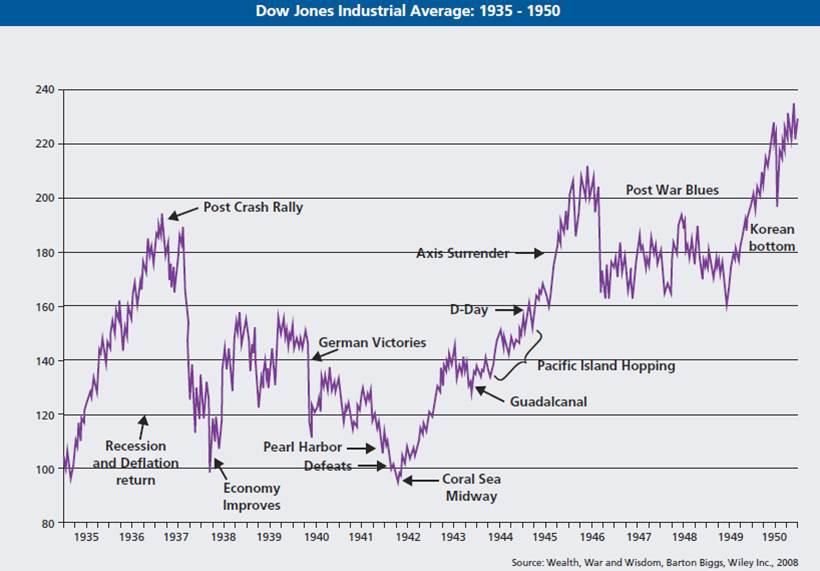

World War II (1939-1945)

The market's reaction to World War II was more nuanced and provides an even clearer illustration of its forward-looking nature.

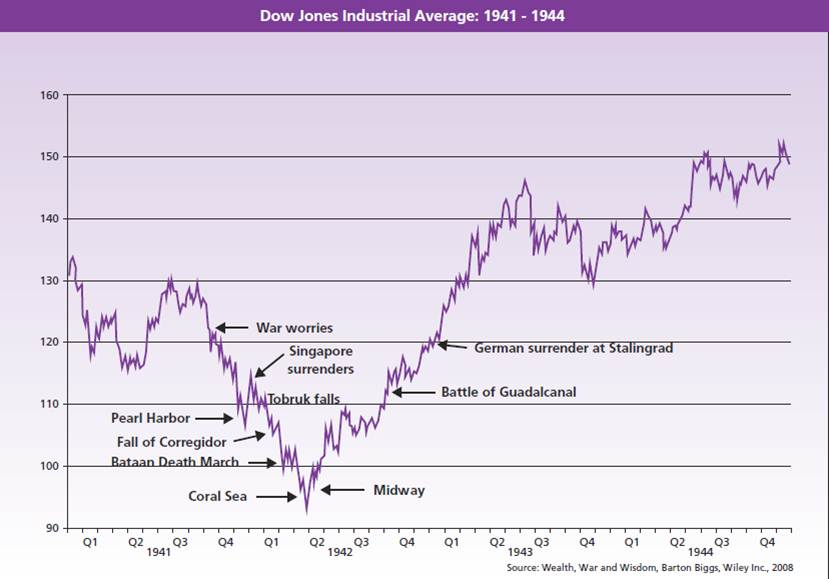

Initial Reaction and the "War Puzzle": Unlike the surprise of 1914, the outbreak of war in Europe had been widely anticipated. When Hitler invaded Poland on September 1, 1939, the market's reaction was not panic, but relief that the uncertainty was over. On the next trading day, the Dow jumped nearly 10%. This is a classic example of the "war puzzle," where the arrival of a long-feared event can be bullish as it allows investors to price a known reality rather than an infinite number of potential negative outcomes.

U.S. Entry and the Market Bottom: The surprise attack on Pearl Harbor on December 7, 1941, which thrust the U.S. directly into the conflict, triggered the expected negative reaction. The Dow fell 2.9% on the following trading day, and the S&P 500 experienced a total drawdown of 19.8% over the subsequent 143 days. Yet, the initial losses from the attack itself were recovered in less than a month.

Overall Performance and International Divergence: From that 1942 low, the U.S. market embarked on a powerful bull run that continued through the war's end. When the Allied forces invaded France on D-Day in June 1944, the market barely registered the event, rising over 5% in the following month. For the entire war period, from 1939 to 1945, the DJIA posted a total gain of 50%, an annualized return exceeding 7%.

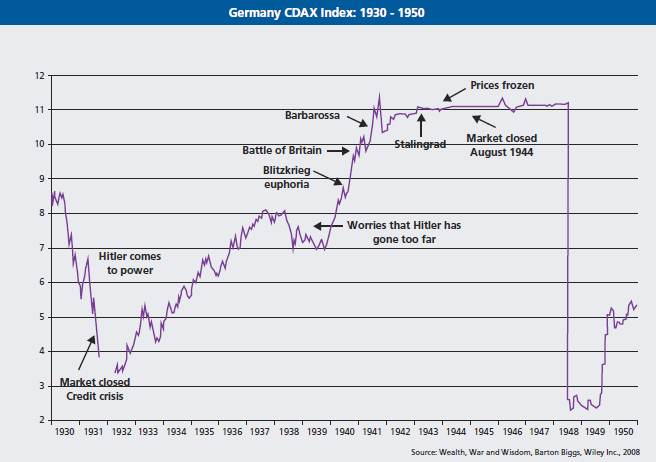

This positive performance was, however, exclusive to the victors. The markets of the losing powers were annihilated. Between 1939 and 1947, German stocks lost 90% of their real value, while Japanese stocks lost a staggering 99%.6 The German stock market itself had displayed a similar prescience to its American counterpart; after booming on military production through 1941, the Berlin market peaked in the late fall of that year, seemingly sensing that Germany's military momentum had crested and its fortunes were about to turn.7 This stark divergence underscores a crucial lesson: stock market performance during a war is critically dependent on being on the winning side and, most importantly, on avoiding the direct destruction of one's domestic capital stock.

The performance of the U.S. market during World War II was not merely a story of increased defense spending. It was the story of a fundamental economic regime change. The immense fiscal stimulus of the war effort effectively ended the lingering Great Depression, pulling millions into the workforce, driving technological innovation, and unleashing productivity gains that would power decades of post-war prosperity. The market, in its rally from 1942 onward, was not just pricing in an Allied victory; it was pricing in the birth of the post-war American economic superpower, a world in which the U.S. industrial base would be left unrivaled while its competitors lay in ruins. This context is critical: applying the WWII market analogy to modern, limited conflicts is deeply flawed unless the conflict is similarly transformative for the underlying structure of the global economy.

The Cold War and Its Proxies - From Korea to Vietnam

The Cold War era, characterized by ideological struggle and proxy conflicts rather than direct great power confrontation, offers a different set of lessons. The market performance during the wars in Korea and Vietnam provides a powerful case study in how the economic and policy response to a conflict is a far more critical driver of returns than the battlefield events themselves. The stark contrast between these two conflicts demonstrates the primacy of sound fiscal and monetary policy in shaping investor outcomes.

Korean War (1950-1953)

When North Korean forces stormed into South Korea on June 25, 1950, the surprise was total and the market's initial reaction was severe. The S&P 500 fell 5.38% on the first trading day after the invasion, and the Dow suffered its worst one-day drop since 1937 and its worst weekly decline since the 1930s. The total drawdown for the S&P 500 reached 12.9%.11

This initial panic, however, quickly gave way to a powerful bull market. Several factors contributed to this rapid reversal. The U.S. economy in 1950 was fundamentally strong, still benefiting from the post-WWII boom and with relatively low inflation.8 Crucially, the Truman administration and Congress made the decision to finance the war effort largely on a "pay-as-you-go" basis through significant increases in personal, corporate, and excise taxes.9 This fiscally responsible approach, combined with an anti-inflationary monetary policy from the Federal Reserve, prevented the kind of economic overheating that can derail a market rally. The war boosted GDP growth through government spending without unleashing runaway inflation.

The market results were impressive. By the time the war ended in July 1953, the Dow had risen by nearly 60% from its pre-war level, an annualized gain of 16%. The S&P 500 was up almost 30% over the same period. For the calendar year 1950 alone, despite the shock of the invasion, the S&P 500 finished up 31.7%.10 The Korean War demonstrated that a major military conflict, if managed with fiscal prudence in the context of a strong underlying economy, can be decidedly bullish for stocks.

Vietnam War (1965-1973)

The Vietnam War provides a stark and instructive contrast. The market's reaction to this long, divisive conflict was far more muted and volatile. When the first major contingent of U.S. combat troops arrived in 1965, the Dow actually closed the year with a 10% gain. Even the 1968 Tet Offensive, a major military escalation, prompted a relatively mild 6% drawdown in the S&P 500.

Year | S&P 500 Annual Return (%) | Key Events12 |

1965 | +12.5% | Major U.S. troop deployment begins |

1966 | -10.1% | War escalates; inflation concerns grow |

1967 | +24.0% | Market rebounds amid economic growth |

1968 | +11.1% | Tet Offensive occurs; market shows resilience |

1969 | -8.5% | "Guns and butter" spending fuels inflation |

1970 | +4.0% | Mild recession hits U.S. economy |

1971 | +14.3% | Market recovery |

1972 | +19.0% | Continued market gains |

1973 | -14.7% | U.S. involvement ends; oil crisis begins |

The problem for the market was not the war itself, but how it was paid for and the economic environment in which it occurred. Unlike the Korean War, the Vietnam War was financed not with tax increases but with massive government borrowing. This deficit spending was layered on top of the expensive domestic "Great Society" programs, a policy mix often referred to as "guns and butter". This combination of immense fiscal stimulus in an economy already near full employment was profoundly inflationary. The war spending helped kick off the "Great Inflation" of the 1970s and contributed to a mild recession in 1970.

The market's performance reflected this difficult macroeconomic backdrop. While the Dow did grow by a total of 43% over the long 1965-1973 period (an annualized rate of about 5%), this headline number masks significant volatility, deep drawdowns, and poor inflation-adjusted returns. Indeed, some analyses identify the Vietnam War era as a notable exception to the general rule of stocks performing well during wartime, with returns falling below their long-term historical average.13

The divergence between the Korean and Vietnam War outcomes offers a critical analytical insight. For investors assessing a new conflict, the most predictive questions are not about military strategy or battlefield momentum. Instead, they are: "How is the war being financed?" and "What is the likely impact on inflation and interest rates?" The Korean experience shows that a war funded by taxes can be sustained without destabilizing the economy. The Vietnam experience shows that a war funded by debt during an inflationary period creates a toxic environment for equity investors. This framework, focused on the primacy of fiscal and monetary policy, is far more useful for forecasting market direction than tracking the ebb and flow of the conflict itself.

Modern Conflicts - Energy, Terrorism, and Regional Instability

The post-Cold War era has been defined by a different character of conflict: regional wars often centered on resource control, asymmetric warfare waged by non-state actors, and the increasing use of economic sanctions. The market's reaction to these events reveals a system that has become progressively more adept at absorbing geopolitical shocks, with recovery times shortening. The primary transmission mechanism for these modern conflicts to impact global markets has been through their effect on commodity prices—especially oil—and their tendency to exacerbate pre-existing economic vulnerabilities.

The Gulf Wars and the Centrality of Oil

The Iraqi invasion of Kuwait in August 1990 provided a clear example of a geopolitical shock triggering a market downturn by hitting a key economic pressure point: energy prices. The invasion caused the price of crude oil to nearly double, from around $20 to $40 per barrel. This oil shock, occurring alongside the domestic Savings and Loan crisis, tipped the U.S. economy into a brief recession. The S&P 500 reacted with a significant 16.9% correction that lasted 71 days before bottoming.

The market's behavior during the 2003 Iraq War was markedly different and serves as a textbook illustration of the "war puzzle." In the months leading up to the invasion, markets were weak, pricing in the uncertainty of the looming conflict. However, once the U.S.-led military action commenced in March 2003, resolving that uncertainty, the market began a powerful rally. The DJIA surged 8.4% in the month following the start of the invasion, and the S&P 500 finished the year up an impressive 26.4%. Investors, anticipating a swift and successful military campaign, effectively "bought the invasion." Both conflicts underscored the immense strategic importance of Gulf oil producers, particularly Saudi Arabia, as the swing producers capable of stabilizing the global energy market.

The Russia-Ukraine War: An Inflation Amplifier

The 2022 Russian invasion of Ukraine is a quintessential case study of a geopolitical event acting as an amplifier for existing negative economic trends. By early 2022, global inflation was already elevated due to post-pandemic supply chain snarls and massive fiscal stimulus. The war then poured fuel on this fire.

Russia and Ukraine are both critical global suppliers of a wide range of commodities, including oil, natural gas, wheat, barley, corn, and industrial metals. The invasion and subsequent sanctions triggered a massive spike in the prices of these goods, driving global inflation to multi-decade highs. This, in turn, likely forced central banks, including the Federal Reserve, to pursue a more aggressive path of interest rate hikes than they might have otherwise, creating a severe headwind for financial assets. The S&P 500 fell into a correction, dropping more than 10% from its peak, with the initial impact felt most severely in European markets due to their geographic proximity and dependence on Russian energy.14

Yet, even in the face of this significant economic shock, the market's underlying resilience eventually shone through. As the world adapted—rerouting energy flows, finding new sources of supply, and building new infrastructure—the acute phase of the commodity shock passed. The S&P 500 bottomed in October 2022 and subsequently entered a new bull market, having effectively moved on from the war's direct economic impact long before the conflict itself ended.

Terrorism and Short-Lived Shocks: The Case of 9/11

The September 11, 2001 terrorist attacks represent the archetype of a sudden, horrific, and surprising geopolitical shock. The immediate impact was a four-day closure of the U.S. stock market. When it reopened, the DJIA plunged 7.1% in a single day, one of its largest point declines ever. The total drawdown for the S&P 500 reached 11.6% over the 11 days following the attacks. The event's impact was magnified because it struck an economy already weakened by the bursting of the dot-com bubble, tipping it deeper into recession.

Despite the profound psychological and economic shock, the market's recovery was remarkably swift. The S&P 500 regained all of its losses within just 31 trading days. This rapid rebound demonstrates a key pattern of modern markets: they are adept at processing surprise shocks that, while tragic, do not lead to a prolonged and systemic disruption of the core economic system.

A crucial theme emerges from analyzing these modern conflicts: the "learned resilience" of the market. A generation of investors has now lived through the 9/11 attacks, the 2008 Global Financial Crisis, the European debt crisis, and the COVID-19 pandemic. In each instance, those who panicked and sold into the crisis were punished, while those who held on or "bought the dip" were richly rewarded. This repeated positive reinforcement has conditioned market participants to view geopolitical shocks as temporary dislocations and potential buying opportunities, rather than as paradigm-shifting events that warrant a permanent exit from risk assets. This behavioral adaptation creates a powerful self-reinforcing cycle: investors expect a quick recovery, so they buy into weakness, which in turn helps create the quick recovery. This helps explain why markets can shrug off events like the direct missile exchanges between Israel and Iran in 2024 and 2025 with such speed. Consequently, the threshold for a geopolitical event to cause a sustained bear market is now significantly higher. It would likely require a shock so profound that it fundamentally breaks this "this too shall pass" narrative—most likely by triggering a severe, undeniable global recession or a systemic financial crisis for which there is no immediate policy remedy.

Event | Event Date | S&P 500 Initial 1-Day Reaction (%) | Max Drawdown (%) | Days to Market Bottom | Days to Full Recovery | S&P 500 1-Year Forward Return (%) |

Pearl Harbor Attack | 12/7/1941 | -3.8% | -19.8% | 143 | 307 | 11.4% |

North Korean Invasion | 6/25/1950 | -5.4% | -12.9% | 23 | 82 | 27.4% |

Cuban Missile Crisis | 10/16/1962 | -0.3% | -6.6% | 8 | 18 | 32.1% |

Yom Kippur War | 10/6/1973 | 0.3% | -0.6% | 5 | 6 | -41.1% |

Iraq's Invasion of Kuwait | 8/2/1990 | -1.1% | -16.9% | 71 | 189 | 14.0% |

9/11 Terrorist Attacks | 9/11/2001 | -4.9% | -11.6% | 11 | 31 | -11.2% |

Iraq War Begins | 3/19/2003 | 2.3% | N/A (Rally) | N/A | N/A | 15.6% (from event) |

Russia Invades Ukraine | 2/24/2022 | -2.1% (from 2/17) | -6.8% | 13 | 23 | -1.7% |

Averages | -1.1% | -4.6% | 19 | 40 | 7.8% |

1 https://www.investopedia.com/solving-the-war-puzzle-4780889

4 https://awealthofcommonsense.com/2020/01/the-relationship-between-war-the-stock-market/

5 https://en.wikipedia.org/wiki/Dow_Jones_Industrial_Average

6 https://www.barclaypearce.com.au/blog/absi-how-do-stock-markets-react-to-war

8 https://www.ebsco.com/research-starters/history/korean-wars-impact-us-business

9 https://navellier.com/6-24-25-how-do-markets-react-to-the-outbreak-of-major-wars/

11 https://www.aaii.com/investor-update/article/16252-stock-market-returns-following-military-conflicts

13 https://blogs.cfainstitute.org/investor/2017/08/29/u-s-capital-market-returns-during-periods-of-war/